Your financially secure future starts today

Will your retirement outlast your savings?

Whether you’re 25 or 55, it is vital to seriously consider a proper saving plan to allow for a comfortable and financially secure life after retirement. We understand it can be tempting to put saving for retirement on the back burner when you have other top-of-mind financial concerns like paying down existing debt, lack of emergency savings and inability to meet monthly expenses. But the longer you put off planning for your future, the farther you will fall behind. It’s never too late to start!

Top 6 retirement obstacles

An important step to making the right changes to your retirement plan is knowing what obstacles you are facing. Watch this video highlighting the latest findings on what people are saying their top obstacles are for retirement savings.

New opportunities to save smarter

Recent changes in retirement and savings rules could make it easier for you to build financial security – whether you're saving for retirement, preparing for emergencies or paying off student loans. Here are a few key updates that may benefit you:

- No more RMDs from Roth 401(k)s – You’re no longer required to take required minimum distributions (RMDs) from workplace Roth accounts, allowing your savings to grow tax-free even longer.

- Higher catch-up contributions for older workers – If you're nearing retirement, you may be eligible to contribute more to your 401(k) or other qualified accounts.

- Emergency savings built into retirement plans – Employers can now offer penalty-free emergency savings accounts within defined contribution plans.

- Student loan repayment rewards – Employers can match employees’ student loan payments with contributions to their retirement account.

- 529 rollovers to Roth IRAs – It’s now easier to transfer unused college savings into a Roth IRA, helping you repurpose funds for long-term goals.

We are living longer so does that mean we need to work longer?

Not necessarily. You can start saving early.

One of the biggest impacts on your retirement savings is when you start. Even if you are not able to contribute the recommended amount each year (10-15% pre-tax salary), starting at a young age will result in greater savings from time and compounding. Check out this example of the exponential effect time and compound interest has on your retirement savings.

THE POWER OF COMPOUND INTEREST

The earlier a person starts saving for retirement, the more time that money has to grow.

| Age of Investment |

25-65 years |

35-65 years |

25-35 years |

25-65 years |

| Amount Invested |

$200/month |

$200/month |

$200/month |

$200/month |

| Earning % |

6.25% |

6.25% |

6.25% |

2.0% (savings) |

| Principal Invested | $96,000 | $72,000 | $24,000 | $96,000 |

| Total Accumulations |

The above example is for illustrative purposes only and not indicative of any investment. Source: J.P. Morgan Asset Management, Retirement Insights, Guide to Retirement, 2022.

If you plan to retire at age 65, you should SAVE ABOUT 12x your annual salary.1

Learn and plan your retirement

We at USI Consulting Group (USICG) have a robust library of retirement and investment resources to help educate and assist retirement plan participants in managing their retirement accounts and setting a plan to reach their post-work life goals.

Make sure you are participating in your employer-sponsored retirement plan to start saving for your future!

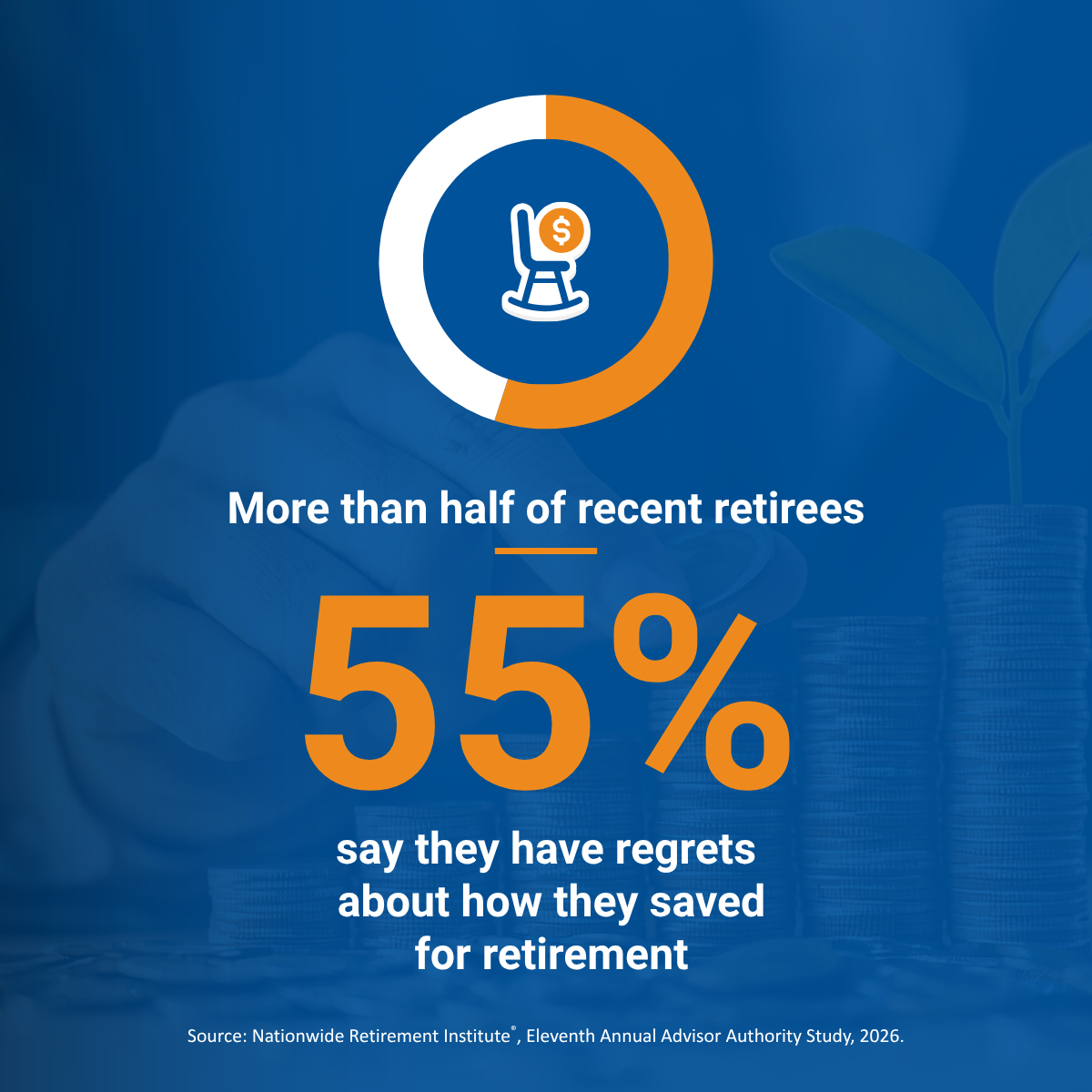

Why should employers care about employee retirement readiness?

Financial wellness in the workplace isn’t just about offering a retirement plan – it’s about ensuring your employees are truly prepared to retire. When employees struggle with short-term financial challenges like debt, emergency savings or healthcare costs, long-term goals like retirement often fall by the wayside.

|

|

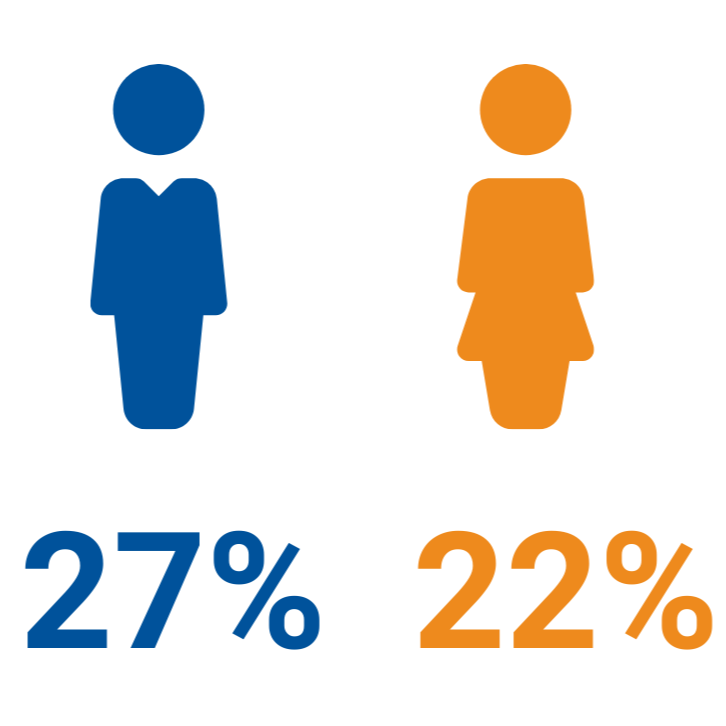

Only 27% of men and

|

Even if your employees aren’t asking for help, they need more than calculators and one-off sessions with investment specialists. They need a comprehensive financial wellness program that helps them:

|

|

Why it matters to your business: When employees aren’t financially prepared to retire, it can have a direct impact on your bottom line. Read our article, Is Delayed Retirement Impacting Your Organization’s Bottom Line?, to learn about the impacts of delayed retirement. Employers may spend an additional $103,000 per employee, per year when retirement is delayed.3 The ripple effects include:

+ |

|

|

Higher labor costs & more paid time off |

+ |

|

|

Increased healthcare premiums |

= |

|

|

Lower productivity |

By helping employees improve their financial well-being and retirement readiness, you’re not just supporting their future – you’re strengthening your organization today.

Help your employees retire with confidence

For more than 50 years, USI has helped organizations strengthen their retirement programs and empower employees to make informed financial decisions. Through strategic consulting, fiduciary guidance, participant education and integrated retirement plan solutions, we help employers optimize plan outcomes, enhance employee engagement and improve retirement readiness. Contact your USI Retirement representative, visit our Contact Us page or email us at information@usicg.com to learn more.

![]()

1 Fidelity Viewpoints, How much do I need to retire?, February 2025

2 Bank of America, Employee Financial Wellness in 2025

3 Principal, Cost of Retirement Analysis, September 2025

This information is provided solely for educational purposes and is not to be construed as investment, legal or tax advice. Prior to acting on this information, we recommend that you seek independent advice specific to your situation from a qualified investment/legal/tax professional. | 1023.S1012.0077