Market & Legal Update

May 2024

Market Update | A May Rebound

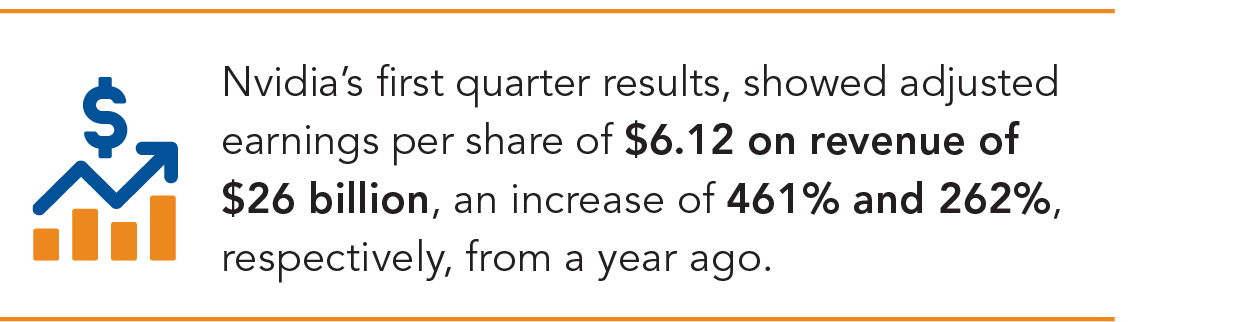

Following a rough month of April for the markets, May was a welcomed relief. The U.S. stock market set aside worries about interest rates remaining high in part because stocks related to artificial-intelligence technology continue to climb. Nvidia's first quarter results, released after the bell on May 22nd, showed adjusted earnings per share (EPS) of $6.12 on revenue of $26 billion, an increase of 461% and 262%, respectively, from a year ago. That’s certainly not to say the markets ignored inflation data, but that data wasn’t weak enough to take the wind out of the market’s sails. The Dow Jones Industrial Average (DJIA) gained 2.6% for the month while the S&P 500 tacked on 5.0%. The tech-intensive NASDAQ jumped 6.9%. Longer-term bond yields dropped, with the 10-year treasury falling from 4.68% to 4.51%, causing bond prices to rise. The Barclay’s U.S. Aggregate Index gained 1.7% for the month.

| Market Return Indexes | May 2024 | YTD 2024 | 2023 |

|---|---|---|---|

| Dow Jones Industrial Average | 2.6% | 3.5% | 16.2% |

| S&P 500 | 5.0% | 11.3% | 26.3% |

| NASDAQ (price change) | 6.9% | 11.5% | 43.4% |

| MSCI Eur. Australasia Far East (EAFE) | 4.0% | 7.5% | 18.2% |

| MSCI Emerging Markets | 0.6% | 3.5% | 9.8% |

| Bloomberg High Yield | 1.1% | 1.6% | 13.4% |

| Bloomberg U.S. Aggregate Bond | 1.7% | -1.6% | 5.5% |

| Yield Data | May 2024 | April 2024 | March 2024 |

| U.S. 10-Year Treasury Yield | 4.51% | 4.68% | 4.20% |

U.S. economic data was a bit mixed in the month of May. Back in April, rather disappointing first quarter GDP growth data was released, as economists had forecasted 2.5% GDP growth for Q1, but the first estimate came in at a much lower 1.6%. Markets reacted very negatively to the data with fears of stagflation, and even recession, coming back into play. So, when the second estimate of Q1 GDP growth was released on May 30th and showed that number revised even lower, to 1.3%, markets tumbled. The reduced estimate was primarily due to a downward revision to consumer spending, per the Bureau of Economic Analysis (BEA). Personal consumption in the first quarter grew at 2.0%, down from a prior reading of 2.5%. While the data was certainly disappointing, it’s not at all surprising that the economy slowed a bit this year considering the Federal Reserve instituted 525 basis points worth of interest rate hikes since March 2022 to combat inflation. The good news, so to speak, is that the labor market remains resilient with continued positive job growth and a low unemployment rate. Meanwhile, consumer spending also remains relatively healthy.

Speaking of the consumer, U.S. consumer confidence had declined for three straight months through April and analysts expected much of the same in May. Yet consumer confidence rose in May amid optimism about the labor market, despite the consumer remaining anxious about inflation and interest rates. The Conference Board’s data, released on May 28th, showed that the consumer confidence index, which measures both Americans’ assessment of current economic conditions and their outlook for the next six months, rose in May to 102.0 from 97.5 in April. While the data showed that more consumers believed that the economy could slip into recession in the next 12 months, consumers were also very upbeat about the stock market and labor market improvements.

Likely the most impactful data related to market movement was the April inflation data. Consumer Price Index (CPI) data showed that prices increased less than expected, suggesting that inflation resumed its downward trend at the start of the second quarter. CPI increased 0.3% for the month and was up 3.4% year-on-year. Core CPI, which strips out the volatile food and energy component, was up 0.3% for the month and 3.6% year-on-year. The Fed’s preferred inflation gauge, the core Personal Consumption Expenditures (PCE) index, which strips out the cost of food and energy, rose 0.2% in April, which was slower than the 0.3% increase seen in March.

While the inflation numbers showed improvement, until Fed officials are convinced that inflation is consistently easing, we could see the Fed maintaining rates at current levels for an indefinite period of time. The Fed decided to keep its benchmark interest rate target range at 5.25%-5.50% as it continues its quest to bring inflation down to its goal of 2%. Moreover, minutes from that meeting released a few weeks ago indicated that some policymakers discussed their willingness to raise rates “should risks to inflation materialize in a way that such an action became appropriate”. As such, hopes for a rate cut this year are quickly shrinking as investors have now reduced the odds of the potential first rate cut in September, with a 50% chance the Fed will not cut rates that month. Odds of a cut in November are 46%. While higher rates continue to weigh on the minds of investors, inflation data needs to move in the right direction consistently for the Fed to consider easing interest rates. Whether that occurs this year or next remains to be seen.

Legal Update | Big Changes to Form 5500 for the 2023 Filing Season

As part of the first SECURE Act that was made law back in 2019 the Department of Labor (“DOL”), Internal Revenue Service (“IRS”) and the Pension Benefit Guaranty Corporation (“PBGC”) were directed to make modifications to the 5500 Form, and they complied with that directive by issuing a new regulatory package back in February of 2023. Then earlier this year the agencies released new Form 5500 with instructions which are applicable for filings applicable to plan years beginning on and after January 1, 2023. This article will discuss these changes.

![]()

Participant Counting for the Small Plan Audit Exception

The first big change impacts who must file an accountant’s report with their 5500 series filing. ERISA provides an exemption to small plans with under 100 participants from the requirement to have an annual audit. Before the 2023 filing year, the 5500 instructions defined participants as anyone eligible to participate in the plan, beginning in 2023 defined contribution plans only need to count individuals that have account balances in the plan at the beginning of the year as a participant for determining the small plan audit exemption. Essentially this change is going to provide some small 401(k) and 403(b) plans with a little more breathing room before the audit requirement kicks in. Brand new plans will need to count the number of participants at the end of the initial plan year.

![]()

Administrative Expenses Reported on Schedule H

Schedule H to Form 5500 requires the disclosure of certain financial information about a Plan. The 2023 version of Schedule H will require new breakout categories of administrative expenses that provide significantly more detail about things like recordkeeping fees, auditor fees, actuarial fees, trustee fees to be disclosed on Schedule H. Previous versions of Schedule H lumped these fees into 5 categories, going forward there are 12 separate categories. This detail going into the 5500 will not only mean the DOL will have more access to plan expense information, but also this data will be publicly accessible.

![]()

Retirement Plan Information on Schedule R

Schedule R has been modified to add several new compliance questions including:

- Whether the plan uses permissive aggregation.

- Whether it is a designed based safe harbor 401(k) plan.

- Whether the plan is using current or prior year for ADP testing.

- If the plan is using a pre-approved document, then the document opinion letter date and serial number must be disclosed.

Schedule R also now requires defined benefit plans with 1,000 or more participants at the beginning of the plan year to disclose some specific funding information. Line 19 of this form now requires the plan’s asset holdings be broken into seven specified asset classes held at the end of the plan year and each class will be reported as a percentage of the total plan assets.

![]()

New Schedule MEP for Multiple Employer Plans

A new Schedule MEP has been added to facilitate information reporting for multiple employer plans (MEPs) and a new type of plan created by SECURE 2.0, Pooled Employer Plans (PEPs). Information for MEPs on this schedule had previously been reported on an attachment to Form 5500 and included information broken down and presented for each participating employers (including their percentage of total contributions and aggregate account balance information).

Schedule MEP also includes questions related to PEPs and compliance with the pooled plan provider registration form that has been dubbed Form PR. The Schedule also records the type of multiple-employer plan involved – whether a pooled employer plan, association retirement plan, professional employer organization (“PEO”) or other multiple employer plan – with specific MEPs required to complete identified sections.

![]()

New Schedule DCG for Defined Contribution Retirement Plan Groups

The first SECURE Act (SECURE Act of 2019) added a new type of consolidated Form 5500 filing option for multiple plans that participate in a “defined contribution group” (or “DCG”).

To be eligible to file a consolidated Form 5500 as a DCG, a group of defined contribution plans must have the SAME:

![]()

Administrator

![]()

Named fiduciaries

![]()

Trustee

![]()

Plan year

![]()

Investments or investment options

A Schedule DCG must be attached to Form 5500 for each individual plan within the DCG. The Schedule DCG provides individual plan-level information for each participating entity within the group, including participant counts, financial information, and compliance questions.

DCGs are generally subject to the Form 5500 requirements for large pension plans. Each plan within the group that is subject to an audit requirement, which is determined on a plan-level, must attach the auditor’s report to the Schedule DCG.

![]()

Defined Benefit Funding Disclosures

Schedule SB, for single employer defined benefit plans and Schedule MB for multiemployer pension plans have been modified to include additional funding information.

![]()

Administrative Penalties

These Form 5500 revisions for 2023 are the most significant changes that plan administrators have seen any many years. Plan sponsors need to be aware of the changes to file complete and accurate 5500s. To bring the importance of these filings home the 2023 instructions to Form 5500 also reflect the significant increase in the maximum civil penalty amount for noncompliance assessable under ERISA. Currently, the DOL has the authority to assess civil penalties of up to $2586 per day against a plan administrator that fails to file a complete or accurate Form 5500, and that figure can now increase every year. Additionally, the IRS has its own penalty structure of $250 per day up to a maximum of $150,000 (the maximum was previously $15,000) for failing to file a Form 5500 in the case of a qualified plan.

How USI Consulting Group (USICG) Can Assist

Most retirement plans will be impacted by the new Form 5500 changes and the USICG team is happy to assist employers with these changes as well as any other retirement plan compliance matters. USICG will continue to provide any relevant developments relating to government reporting and disclosure requirements. To learn more, please contact your local USICG representative.

Retirement Resources for You

USI Consulting Group's team of experts is happy to assist employers with all retirement plan compliance matters and changes in the market, including those discussed here, to help you mitigate risk and financial impact to your organization.

Questions? Contact your USICG representative, visit our Contact Us page or reach out to us directly at information@usicg.com.

Find the address and telephone number of your local USI Consulting Group office here.

![]()

Print this May 2024 Market & Legal Update

For previous market and legal commentaries please click here.

This communication is published for general informational purposes and is not intended as advice or a recommendation specific to your plan. Neither USI nor its affiliates and/or employees/agents offer legal or tax advice.

An index is a measure of value changes in a representative grouping of stocks, bonds, or other securities. Indexes are used primarily for comparative performance measurement and as a gauge of movements in financial markets. You cannot invest directly in an index and, for comparative purposes; they do not reflect the effect of the various fees inherent in actual investment vehicles.

The S&P 500 Index is a market value weighted index showing the change in the aggregate market value of 500 U.S. stocks. It is a commonly used measure of stock market total return performance.

The Dow Jones Industrial Average is a price weighted index comprised of 30 actively traded blue chip stocks; primarily industrial companies, but including some service oriented firms.

The NASDAQ Composite Index is a market-value weighted index that measures all domestic and non-U.S. based securities listed on the NASDAQ Stock Market.

Gross Domestic Product (GDP) is the market value of the goods and services produced by labor and property in the U.S. It is comprised of consumer and government purchases, net exports of goods and services, and private domestic investments. The Commerce Department releases figures for GDP on a quarterly basis. Inflation adjusted GDP (or real GDP) is used to measure growth of the U.S. economy.

The MSCI Europe and Australasia, Far East Equity Index (EAFE) is a market capitalization weighted unmanaged index developed by Morgan Stanley Capital International to measure approximately 1,100 securities in 21 major overseas stock markets. It is a commonly used measure for foreign stock market performance.

The Barclays Capital U.S. Aggregate Index covers the U.S. Dollar denominated investment grade, fixed-rate, taxable bond market of SEC-registered securities.

The Barclays Capital U.S. Corporate High Yield Index covers the U.S. Dollar denominated, non-investment grade, fixed income, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s Fitch, and S&P is Ba1/BB+/BB+ or below.

The MSCI Emerging Markets Index (EM) is a free-float-adjusted market-capitalization index developed by Morgan Stanley Capital International. It is designed to measure the equity market performance of 26 emerging market countries.

The 10 Year Treasury Yield is the interest rate the U.S. government pays to borrow money for a 10-year period. In addition to influencing how much the government pays to borrow over this time-frame, the 10-year Treasury Yields also determines how much investors earn by investing in this debt and it is a good indicator of investor sentiment The higher the yield, the better the economic outlook.

Market Update is a monthly publication circulated by USI Advisors, Inc. and is designed to highlight various market and economic information. It is not intended to interpret laws or regulations.

This report has been prepared solely for informational purposes, based upon information generally available to the public from sources believed to be reliable, but no representation or warranty is given with respect to its completeness. This report is not designed to be a comprehensive analysis of any topic discussed herein, and should not be relied upon as the only source of information. Additionally, this report is not intended to represent advice or a recommendation of any kind, as it does not consider the specific investment objectives, financial situation and/or particular needs of any individual client.

Investment Advice provided by USI Advisors, Inc. Under certain arrangements, securities offered to the Plan through USI Securities, Inc. Member FINRA/SIPC. 95 Glastonbury Blvd., Suite 102, Glastonbury, CT 06033. USI Consulting Group is an affiliate of both USI Advisors, Inc. and USI Securities, Inc. | 5024.S0603.0041

RECENT PUBLICATIONS

- February 2026 | Market & Legal Update 3/4/2026

- January 2026 | Market & Legal Update 2/3/2026

- December 2025 | Market & Legal Update 1/5/2026

Not receiving our newsletter?

Stay up to date with retirement plan updates and insights by subscribing to our email list.